Data released Thursday by Realtor.com and Redfin shows that even as more homes are being listed for sale and mortgage payments are becoming more affordable, fewer transactions are occurring.

According to a housing trends report from Realtor.com, active listings were up nearly 36% year over year in August. It was the 10th straight month of annualized growth and for-sale inventory is now at its highest level since May 2020.

Meanwhile, Redfin reported that recent mortgage rate declines are contributing to lower housing expenses. The median monthly mortgage payment during the four-week period ending Sept. 1 fell to $2,534, which was the lowest figure since January and down nearly $300 from its peak at the end of April.

But more supply and better affordability aren’t resulting in more sales. The average listing last month had spent 53 days on the market, the slowest August in five years, according to Realtor.com. And Redfin data shows that pending sales dropped 8.4% year over year in August — the largest decrease in nearly a year. This dovetails with recent pending sales data from the National Association of Realtors.

“The widely anticipated Fed rate cut has already ushered in lower mortgage rates, but it seems that some buyers and sellers are waiting for additional declines,“ Realtor.com chief economist Danielle Hale said in a statement.

“As the market slows seasonally, fall is one of the best times to buy a house. Falling mortgage rates are likely to bring out additional home shoppers and a busier fall season than usual, but the boost in activity is unlikely to overwhelm the usual seasonal slowdown. Shoppers, who are out this fall, are likely to face lower competition than is expected in spring 2025 as more shoppers anticipate better mortgage rates.”

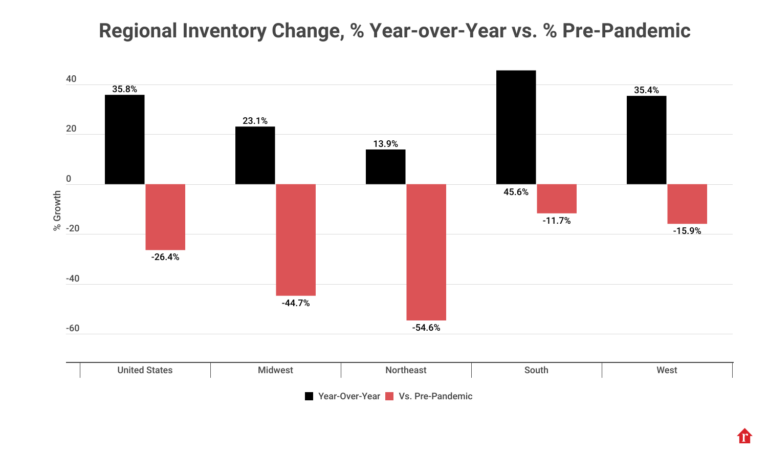

Notably, even as more sellers are entering the market compared to a year ago, for-sale inventory remains markedly below pre-pandemic levels. Realtor.com found that the number of listings at the national level last month was 26.4% less than the average August from 2017 to 2019. The smallest inventory gap compared to the pre-pandemic period was in the South region (-11.7%) while the largest was in the Northeast region (-54.6%)

Affordability metrics are moving in a positive direction for buyers. Median sale prices in August dropped 1.3% year over year to $429,990.

First-time buyers with smaller budgets, in particular, are likely to have more choices. For a seventh straight month, homes priced between $200,000 and $350,000 represented the fastest-growing segment of listings — up 46% year over year, Realtor.com reported.

This was also reflected in the median price per square foot, which rose 2.3% from August 2023, “indicating that the inventory of smaller and more affordable homes continues to grow in share.“

Redfin mentions multiple factors that are influencing the lack of sales in spite of improving affordability. Some buyers believe that mortgage rates will fall further after Federal Reserve policymakers meet later this month. Others are waiting for more clarity on buyer’s agent compensation following recent rule changes. And some may wait until after the November election when more homeownership incentives could emerge.

“There is demand for desirable, move-in ready listings, but some house hunters are in a holding pattern because the industry is in flux,” Van Welborn, a Phoenix-based agent, said in Redfin’s report.

Still, the market may have more activity this fall than usual. Purchase mortgage applications rose slightly at the end of August and are nearing year-ago levels. Redfin noted that its Homebuyer Demand Index, which measures tour requests and other services, rose 4% between July and August, while Google searches for the phrase “home for sale“ rose 6%.